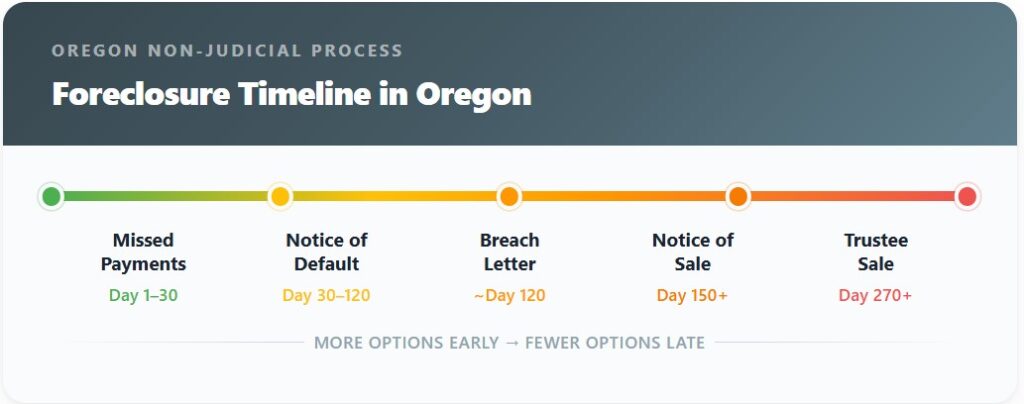

Foreclosure pressure typically begins when a homeowner falls behind on mortgage payments and receives notices from their lender. In Oregon, lenders can pursue either judicial or non-judicial foreclosure, and most residential foreclosures follow the non-judicial path. This process can move relatively quickly once formal notices are filed.

Eugene homeowners in this situation have several potential paths forward. The right choice depends on factors like how much equity is in the home, how far behind payments are, and whether the homeowner wants to keep the property. Understanding each option early gives homeowners the most flexibility.

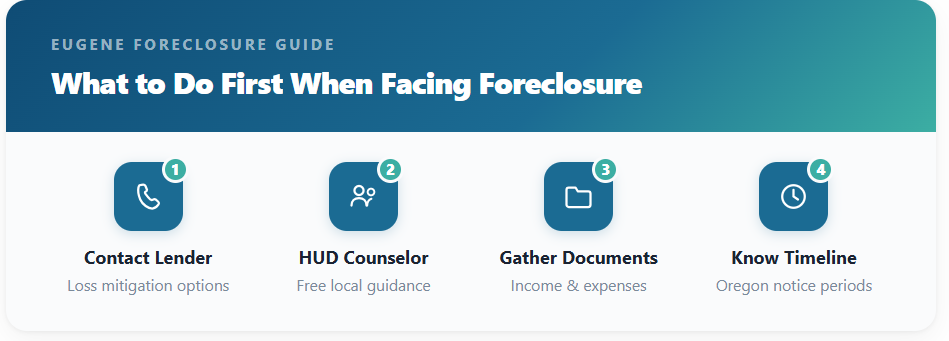

What Should a Eugene Homeowner Do First When Facing Foreclosure?

Contact your mortgage servicer immediately and request a detailed account of what is owed, including any fees that have been added. Early communication with the lender opens the door to potential alternatives before the formal foreclosure process advances further.

Many homeowners delay this step because the situation feels overwhelming. However, most lenders have loss mitigation departments specifically designed to work with borrowers who are behind. The earlier a homeowner reaches out, the more options remain available.

It is also advisable to speak with a HUD-approved housing counselor. Oregon has multiple nonprofit housing counseling agencies, including several that serve the Eugene-Springfield area. These counselors can review a homeowner’s financial situation and help identify which options may be realistic. HUD-approved counseling is available at no cost to the homeowner.

Gathering financial documents early is also important. Lenders and counselors will typically ask for proof of income, a list of monthly expenses, recent bank statements, and any documentation of financial hardship. Having these ready can speed up the process of applying for relief programs or negotiating with the lender.

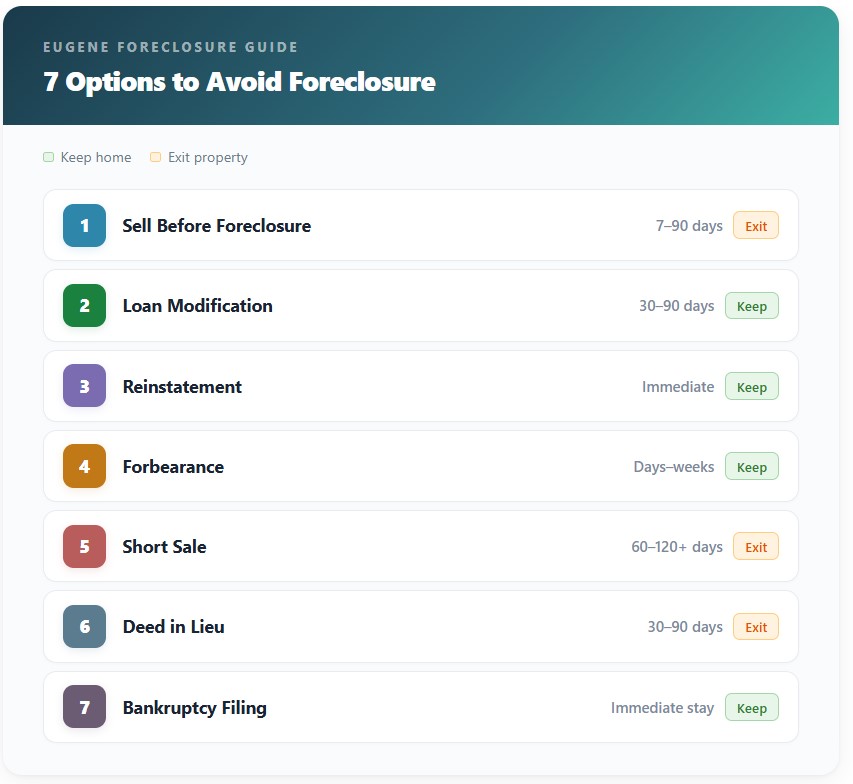

What Options Are Available to Stop or Avoid Foreclosure?

Eugene homeowners facing foreclosure generally have several options, ranging from keeping the home to selling it or negotiating a resolution with the lender. Below is an overview of the most common paths, presented from those that tend to resolve fastest to those that take longer or involve more complexity.

Option 1: Selling the Home Before Foreclosure

How the Process Works

A homeowner lists the property for sale on the open market or sells directly to a buyer before the foreclosure is finalized. If the home has enough equity to cover the remaining mortgage balance, closing costs, and any past-due amounts, the sale pays off the debt and the homeowner keeps any remaining proceeds.

How Quickly It May Help

In most cases, a traditional sale in Eugene takes 30 to 90 days depending on market conditions, pricing, and property condition. Selling to a direct buyer or investor may close in as few as 7 to 21 days, though the sale price may be lower than what the open market would bring.

Advantages

- Avoids a foreclosure on the homeowner’s credit report.

- The homeowner retains control of the sale process and timeline.

- Any equity above the mortgage balance goes to the homeowner.

- Provides a clean resolution without legal proceedings.

Tradeoffs or Risks

- The home must sell before the foreclosure timeline runs out.

- If the home needs repairs, it may be harder to attract traditional buyers.

- A fast sale to an investor may result in a lower price than a full market listing.

Situations Where Homeowners Consider It

Homeowners who have built equity in their property and want to avoid the credit damage of foreclosure often consider selling. This option is especially relevant when the homeowner has already decided they cannot or do not want to keep the property. It is also common when the homeowner needs to relocate or when maintaining the mortgage is no longer financially viable.

Option 2: Loan Modification

How the Process Works

A loan modification changes the original terms of the mortgage. The lender may agree to reduce the interest rate, extend the loan term, or add missed payments to the back end of the loan. The goal is to make the monthly payment more affordable so the homeowner can remain in the home.

How Quickly It May Help

Loan modification applications typically take 30 to 90 days to process. During this period, some lenders may pause foreclosure proceedings, though this is not guaranteed. Homeowners should confirm with their servicer whether a pending application affects the foreclosure timeline.

Advantages

- Allows the homeowner to keep the property.

- May result in a lower monthly payment going forward.

- Avoids the need to sell or vacate the home.

Tradeoffs or Risks

- Approval is not guaranteed. Lenders evaluate income, expenses, and the reason for hardship.

- The total amount paid over the life of the loan may increase if the term is extended.

- Some modifications require a trial payment period before becoming permanent.

Situations Where Homeowners Consider It

This option suits homeowners who want to stay in their home and have experienced a temporary financial setback, such as job loss, medical expenses, or a reduction in income. It works best when the homeowner has recovered or expects to recover financially and can sustain a modified payment.

Option 3: Reinstatement

How the Process Works

Reinstatement means paying the full past-due amount, including any late fees and legal costs, in one lump sum. Once the lender receives this payment, the foreclosure process stops and the original mortgage terms resume as if nothing happened.

How Quickly It May Help

Reinstatement can stop foreclosure almost immediately once payment is received. Oregon law generally allows homeowners to reinstate up until a certain point before the foreclosure sale, though exact deadlines depend on the type of foreclosure and the lender’s timeline.

Advantages

- Stops the foreclosure process quickly.

- Restores the loan to its original terms with no modification needed.

- The homeowner keeps the property and the existing mortgage rate.

Tradeoffs or Risks

- Requires a large lump-sum payment, which many homeowners in financial distress do not have available.

- Does not address the underlying cause of the missed payments.

Situations Where Homeowners Consider It

Reinstatement is most realistic for homeowners who have received a one-time sum of money, such as a tax refund, insurance payout, family assistance, or back pay from an employer. It is less practical for homeowners whose income has permanently decreased.

Option 4: Forbearance Agreement

How the Process Works

A forbearance agreement is an arrangement with the lender to temporarily reduce or pause mortgage payments for a set period. At the end of the forbearance period, the homeowner must repay the missed amounts, either in a lump sum, through a repayment plan, or through a loan modification.

How Quickly It May Help

Forbearance can take effect within days to a few weeks once approved. It provides immediate relief from monthly payment obligations, though the missed payments still need to be addressed later.

Advantages

- Provides short-term breathing room without losing the home.

- Can stop or delay foreclosure proceedings during the forbearance period.

- May be combined with a loan modification afterward.

Tradeoffs or Risks

- Payments are paused, not forgiven. The homeowner still owes the full amount.

- If the homeowner cannot resume payments after the forbearance period, the situation may worsen.

Situations Where Homeowners Consider It

Forbearance is commonly used when a homeowner expects their financial situation to improve within a few months. Examples include temporary unemployment, recovery from illness, or waiting for a pending settlement or benefit payment.

Option 5: Short Sale

How the Process Works

In a short sale, the homeowner sells the property for less than the remaining mortgage balance. The lender must approve the sale because they are agreeing to accept less than what is owed. The homeowner avoids foreclosure, but does not receive any proceeds from the sale.

How Quickly It May Help

Short sales typically take 60 to 120 days or longer, partly because the lender must review and approve the offer. The process can be slower than a standard sale due to this additional layer of approval.

Advantages

- Avoids a foreclosure entry on the homeowner’s credit report, though the short sale itself is noted.

- Allows the homeowner to move on from a mortgage they can no longer afford.

- Generally viewed more favorably than foreclosure by future lenders.

Tradeoffs or Risks

- The homeowner walks away with no equity and may owe taxes on the forgiven debt depending on circumstances.

- The lender may pursue a deficiency judgment for the remaining balance, depending on state law and the terms of the agreement.

- The process is often lengthy and uncertain.

Situations Where Homeowners Consider It

Short sales are most common when the homeowner owes more than the property is worth and cannot afford to continue making payments. This situation can arise when home values have declined since the purchase or when the homeowner took on additional debt against the property.

Option 6: Deed in Lieu of Foreclosure

How the Process Works

A deed in lieu of foreclosure means the homeowner voluntarily transfers ownership of the property to the lender in exchange for being released from the mortgage obligation. The lender takes the property without going through the full foreclosure process.

How Quickly It May Help

This process can take 30 to 90 days to complete, depending on the lender’s requirements and whether the property has any liens or title issues that need to be resolved first.

Advantages

- Ends the foreclosure process without a public auction or court proceeding.

- May have a slightly less negative impact on credit compared to a completed foreclosure.

- Some lenders offer relocation assistance as part of the agreement.

Tradeoffs or Risks

- The homeowner loses the property entirely with no financial return.

- The lender may still seek a deficiency judgment unless specifically waived in the agreement.

- Not all lenders accept a deed in lieu, especially if there are multiple liens on the property.

Situations Where Homeowners Consider It

This path is sometimes pursued by homeowners who have little or no equity, cannot sell the property, and want to avoid the public nature of a foreclosure auction. It is generally considered a last resort after other options have been explored.

Option 7: Bankruptcy

How the Process Works

Filing for bankruptcy triggers an automatic stay, which temporarily halts all collection activity, including foreclosure. Chapter 13 bankruptcy allows homeowners to create a repayment plan to catch up on missed mortgage payments over three to five years while keeping the property. Chapter 7 bankruptcy may delay foreclosure but typically does not prevent it permanently.

How Quickly It May Help

The automatic stay takes effect immediately upon filing. However, Chapter 13 repayment plans must be approved by the court, which can take several months. Bankruptcy remains on a credit report for seven to ten years depending on the chapter filed.

Advantages

- Immediately stops foreclosure proceedings through the automatic stay.

- Chapter 13 allows the homeowner to catch up on payments over time.

- May also address other debts that are contributing to the financial hardship.

Tradeoffs or Risks

- Significant long-term impact on credit history.

- Requires regular income to sustain a Chapter 13 repayment plan.

- Legal fees and court costs add to the financial burden.

- If the homeowner fails to follow the repayment plan, the court may lift the stay and foreclosure resumes.

Situations Where Homeowners Consider It

Bankruptcy is often considered when the homeowner has multiple debts beyond the mortgage and needs a structured way to address them all. It is a significant legal step and typically requires the guidance of a bankruptcy attorney. It is not appropriate for every situation.

How Foreclosure Situations Typically Unfold in Eugene

In Oregon, most residential foreclosures follow the non-judicial process, which is handled outside of court. This process requires the lender to provide a series of notices to the homeowner before a trustee sale can take place. The timeline from the first missed payment to a completed foreclosure can vary but often spans several months.

Eugene’s housing market conditions can affect how foreclosure situations play out for homeowners. In periods of strong buyer demand and limited inventory, homeowners with equity may find it easier to sell their property before foreclosure is finalized. When the market is slower, selling may take longer, which can create tighter timelines.

Lender behavior also varies. Some servicers are more willing to work with borrowers on modifications or forbearance, while others move more quickly through the foreclosure process. The size and type of the lender, the loan type, and whether the loan is federally backed can all influence how much flexibility is available.

Local factors in Eugene and Lane County, such as property taxes, insurance costs, and neighborhood demand, can also shape a homeowner’s options. A property in a high-demand area may attract more buyer interest, while a property needing significant repairs may present additional challenges regardless of market conditions.

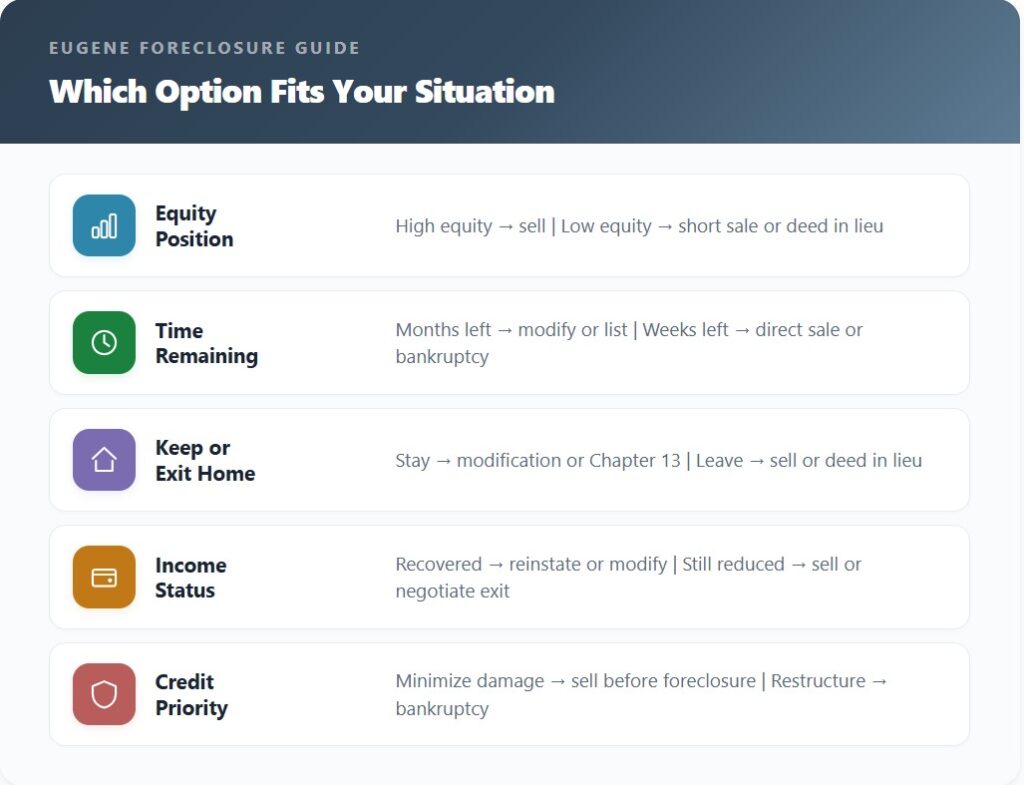

Which Option Is Right Depends on the Homeowner

There is no single foreclosure alternative that works for every homeowner. The right path depends on several individual factors, and what works for one household may not work for another.

Homeowners with significant equity in the property may benefit most from selling, either on the open market or through a direct sale. Those with little or no equity may need to explore short sales or a deed in lieu of foreclosure. Homeowners who want to keep their property and have a stable income may find loan modification or a Chapter 13 repayment plan more appropriate.

The amount of time remaining before the foreclosure sale is also a critical factor. Some options, like reinstatement or a direct sale, can be completed relatively quickly. Others, like loan modification, short sale, or bankruptcy, require more time and may not be available if the foreclosure timeline is nearly complete.

A homeowner’s overall financial picture matters as well. Outstanding debts beyond the mortgage, current income, employment stability, and future financial outlook all influence which options are realistic. Consulting with a HUD-approved housing counselor or an attorney who handles foreclosure cases in Oregon can help homeowners evaluate their situation objectively.

Example of How Some Homeowners Seek Direct Buyers

Some Eugene homeowners facing tight foreclosure timelines choose to work with companies that purchase properties directly. These businesses typically offer a faster closing process than a traditional listing, which can be relevant when time is limited. One example of a company operating in this space locally is orhomebuyers.com, which works with homeowners in the Eugene area.

Direct buyer companies are one of several possible paths and are not suitable for every situation. Homeowners considering this route should compare any offer they receive against the property’s estimated market value and consider consulting with a real estate professional or housing counselor before making a decision.

Frequently Asked Questions

How long does the foreclosure process take in Oregon?

Oregon’s non-judicial foreclosure process generally takes around 120 to 180 days from the filing of the notice of default to the trustee sale, though timelines can vary depending on the lender and any legal challenges. Judicial foreclosures, which go through the court system, typically take longer.

Will foreclosure ruin my credit permanently?

Foreclosure has a significant negative impact on credit, but it is not permanent. A foreclosure entry typically remains on a credit report for seven years. The actual effect on a credit score diminishes over time, especially if the homeowner rebuilds credit through responsible use of other accounts.

Can I sell my house after receiving a foreclosure notice?

Yes, homeowners can generally sell their property at any point before the foreclosure sale is finalized. Selling before the auction allows the homeowner to control the process and potentially preserve some equity. However, the sale must close before the scheduled trustee sale date.

What is the difference between a short sale and a foreclosure?

A short sale is a voluntary sale of the property for less than the mortgage balance, with the lender’s approval. A foreclosure is a legal process in which the lender takes possession of the property due to non-payment. A short sale is generally viewed as less damaging to credit than a completed foreclosure.

Should I hire an attorney if I’m facing foreclosure?

Consulting with an attorney experienced in Oregon foreclosure law is generally advisable, especially if the homeowner is considering bankruptcy, negotiating with the lender, or facing a judicial foreclosure. An attorney can review the homeowner’s legal rights and help identify potential defenses or options that may not be immediately apparent.

Are there any government programs that help homeowners in foreclosure?

Several federal and state programs may be available to homeowners facing foreclosure. These can include FHA loss mitigation options, VA loan assistance for eligible veterans, and state-level programs administered through the Oregon Homeownership Stabilization Initiative or similar agencies. Availability and eligibility requirements change over time, so homeowners should check with a HUD-approved housing counselor for current options.

What happens if I just walk away from the property?

Walking away from a property without resolving the mortgage does not eliminate the debt. The lender can proceed with foreclosure and may seek a deficiency judgment for any remaining balance after the property is sold. The foreclosure will appear on the homeowner’s credit report, and in some cases, the forgiven debt may be treated as taxable income.

Can I negotiate with my lender on my own?

Homeowners can contact their lender’s loss mitigation department directly to discuss options. However, navigating lender requirements and paperwork can be complex. A HUD-approved housing counselor can assist at no cost, and an attorney can provide legal advice if the situation involves potential disputes or significant financial risk.

Hi, I’m Bob Bash, founder of OR Home Buyers, serving the Oregon community since 2017. We provide full-service real estate solutions, specializing in cash purchases for both residential and commercial properties. I started this business to help our community navigate difficult real estate situations with professionalism, ethics, and compassion.

My goal is simple: to make every client feel relieved and happy when their real estate challenges are resolved. Helping people find solutions and peace of mind is what drives me every day.