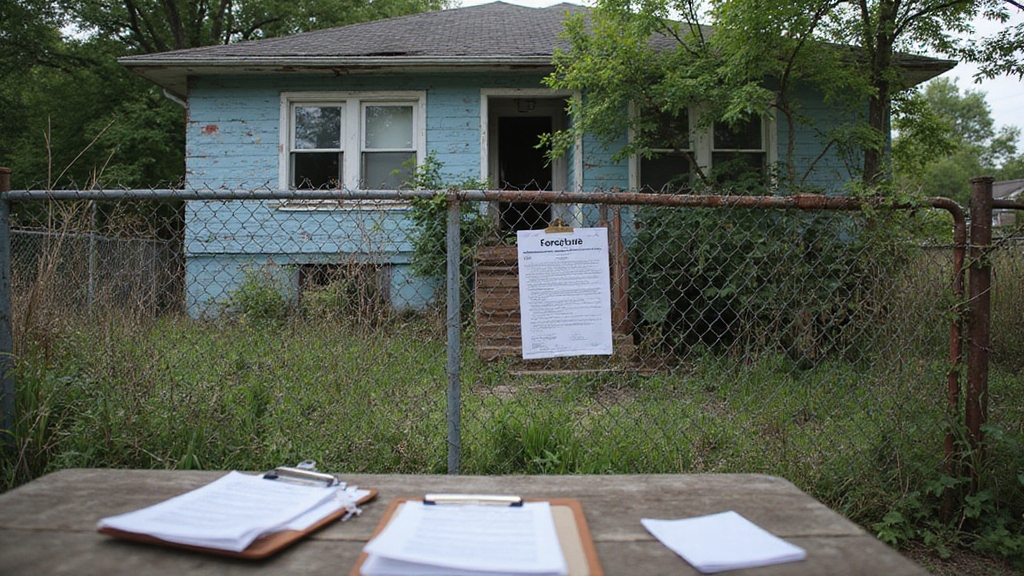

Foreclosure sales can seem like great opportunities for property buyers. Many people assume mortgage companies handle all legal requirements properly before selling. However, title defects and ownership disputes often complicate these transactions more than expected.

According to ORS Chapter 86, Oregon foreclosure sales require clear title, and title defects can actually void sales entirely. Mortgage companies must follow strict legal requirements during the non-judicial process via trustee to ensure proper title transfer.

Buyers face serious financial risks without proper due process and title examination before purchase. This blog post explains how foreclosure sales work, what title problems you might encounter, and how to protect yourself when buying foreclosed homes in Oregon.

Key Takeaways

• Oregon foreclosure sales require clear title under ORS Chapter 86 for valid property transfers

• Title defects and liens can survive foreclosure sales and affect new owners

• Professional title searches and title insurance protect buyers from hidden encumbrances

• Judicial foreclosure in Oregon courts includes a 120-day redemption period under ORS 86

• Lane County experienced 150 foreclosures in 2024, with 20% having tax liens

• Quiet title actions under ORS 86.100 can resolve clouded ownership issues

• Short sales succeed in approximately 40% of cases in Eugene as alternative to foreclosure

What Does Clear Title Mean in Real Estate?

Clear title means property ownership is free from liens, claims, or legal disputes. According to the Oregon Real Estate Agency, no encumbrances can affect ownership rights. The property must have a complete chain of title with proper documentation.

Mortgage lenders verify clear title requirements before approving loans for buyers. Title companies examine public records to confirm legal ownership. Any clouds on title must be resolved before real estate transactions close.

Clear title ensures the seller has full property rights to transfer. Buyers receive complete ownership without hidden debts or claims. Title insurance protects against undiscovered defects after the real estate closing.

What Are the Risks of Buying Foreclosed Properties?

Foreclosed property purchases carry more risks than traditional real estate transactions. Title defects appear frequently in foreclosure sales across Eugene and surrounding areas. Buyers may inherit legal problems from previous owners without proper title examination.

Title Defects and Liens

Eugene data shows that 20% of foreclosed properties have tax liens attached. These title encumbrances often survive the foreclosure process despite the sale. Previous mortgage holders may have recorded multiple liens against the property.

Clouded title issues create legal liability for new owners. Chain of title breaks occur when foreclosure documentation has errors. Invalid foreclosure procedures can result in void title that courts may overturn later.

Outstanding Property Taxes

Property taxes take priority over most other debts in lien priority rules. Counties maintain first position for unpaid tax collections. Outstanding taxes under mechanic’s liens follow ORS 87 regulations in Oregon.

Tax liens transfer to new buyers at foreclosure auctions automatically. Local governments can still foreclose on properties for unpaid taxes. Title insurance may not cover all tax-related title issues buyers inherit.

Undisclosed Ownership Claims

Previous owners may file property ownership disputes after foreclosure sales complete. Family members sometimes claim undisclosed inheritance rights to properties. Mortgage fraud cases can surface years after post-foreclosure sale transactions.

These claims create costly title dispute resolution proceedings for buyers. Courts may side with claimants if wrongful foreclosure occurred. Buyers face legal recourse battles that delay full property marketability.

Mechanic’s Liens and Judgments

Contractors file mechanic’s liens when previous owners didn’t pay for repairs. These liens attach to property regardless of ownership changes. Judgment creditors can place encumbrances that survive some foreclosure sales.

Title searches reveal most liens but hidden claims still emerge. Buyers become responsible for clearing these debts to obtain clear title. Defective title prevents refinancing or resale until all claims are satisfied.

How to Verify Title Status Before Purchasing Foreclosed Property?

Title verification protects buyers from inheriting legal problems with foreclosed homes. Professional services identify title issues before you commit to purchase. Multiple verification steps reduce risks in real estate law compliance.

Order a Professional Title Search

Professional title searches are available through the Lane County Clerk’s office. Title companies examine decades of property records for encumbrances. They trace the complete chain of title to identify gaps or problems.

These searches reveal liens, judgments, and ownership disputes on record. Mortgage servicer responsibilities include some title work during foreclosure process. However, independent verification protects your interests as the buyer.

Review Public Records and Court Documents

County records contain foreclosure documentation and property ownership history. Court filings show pending lawsuits or bankruptcy impact on property rights. These documents reveal whether due process was followed correctly.

Buyers should verify the foreclosure regulations compliance in state foreclosure laws. Check for redemption periods still active under title redemption rights. Review all mortgage default notices and trustee sale announcements carefully.

Hire a Real Estate Attorney

Real estate attorneys understand Oregon foreclosure laws and property buyer protection requirements. They review foreclosure sale documents for compliance with legal requirements. Attorneys identify potential wrongful foreclosure claims before they become your problem.

Legal counsel examines whether mortgage company obligations were properly fulfilled. They assess risks of clouded ownership and title certification issues. Attorney fees cost less than fixing title problems after purchase.

Obtain Title Insurance

Title insurance is mandatory for loans on foreclosed properties in Oregon. Insurance companies conduct their own title examination before issuing policies. They protect against financial losses from undiscovered title defects.

Policies cover legal defense costs for title dispute resolution claims. Lenders require title insurance to protect their mortgage lender rights. Buyers should purchase owner’s policies for complete property rights protection.

What Legal Protections Exist for Foreclosure Sale Buyers?

Oregon provides several legal safeguards for people buying foreclosed homes. State foreclosure laws establish minimum standards for the foreclosure process. Buyers receive certain disclosure requirements and procedural protections under real estate law.

State Foreclosure Laws and Requirements

Oregon foreclosure laws protect buyers through post-foreclosure sale legal requirements. Mortgage companies must follow specific foreclosure regulations before selling properties. Trustees handling sales have legal liability for proper documentation and procedures.

State statutes mandate specific timelines and notice requirements throughout foreclosure. These protections ensure homeowner rights are respected during mortgage default situations. Violations can result in invalid foreclosure that buyers can challenge.

Judicial vs Non-Judicial Foreclosure Processes

Judicial foreclosure occurs through Oregon courts with full legal oversight. Judges review whether mortgage lender rights and mortgage servicer responsibilities were properly executed. Court supervision reduces risks of defective title and procedural errors.

Non-judicial foreclosure uses trustees to conduct property sales without court involvement. This faster process still requires strict compliance with ORS Chapter 86. Buyers get fewer protections but benefit from lower transaction costs.

Right of Redemption Periods

Oregon provides a 120-day redemption period under ORS 86 for certain foreclosures. Previous owners can reclaim property by paying outstanding debts during this window. Buyers must wait for title redemption periods to expire before obtaining marketable title.

Redemption rights affect when title transfer becomes final after foreclosure auctions. Some foreclosure types have longer or shorter redemption periods. Understanding these timelines prevents problems with property ownership disputes later.

Can You Sell a House With Title Issues?

Properties with clouded title can still be sold under certain conditions. Multiple options exist for handling title encumbrances before or during sale. The best approach depends on the specific title defects involved.

Quiet Title Actions

Quiet title actions under ORS 86.100 legally resolve clouded ownership through courts. These lawsuits remove invalid claims and clear defective title from property records. Judges examine evidence and issue orders that establish clear title requirements.

The process takes several months but provides definitive title cure solutions. Courts can eliminate liens without proper documentation or questionable chain of title. Successful quiet title action makes property marketable for traditional real estate transactions.

Selling to Cash Buyers As-Is

Cash sales as-is are possible even with significant title problems. Investors and specialized buyers purchase properties despite title issues at discounted prices. These transactions avoid traditional lending that requires clear title certification.

Cash buyers often handle title dispute resolution after purchase themselves. They calculate risks and adjust offers to account for title encumbrances. This option provides quick property sale without lengthy legal proceedings first.

Working With Title Companies

Title companies help identify specific problems affecting property marketability. They suggest solutions for curing title defects before listing properties. Some issues resolve quickly through simple documentation or quitclaim deed from claim holders.

Title professionals coordinate with attorneys on quiet title action when necessary. They facilitate negotiations with lien holders to release claims. Their expertise speeds up title cure processes for faster property sale.

What Are Your Options If You Own a Property Facing Foreclosure?

Homeowners have several alternatives to completing the full foreclosure process. Acting early provides more options and better outcomes than waiting. Each approach has different impacts on credit and future homeowner rights.

Selling Before Foreclosure Completion

Selling property before foreclosure completion preserves equity and credit ratings. Standard real estate transactions pay off mortgage debt and avoid foreclosure records. Trustee sale avoidance maintains better financial standing for future purchases.

Timing matters because some foreclosure stages limit your legal recourse options. Properties sell faster when marketed before auction dates approach. Buyers prefer homes without active foreclosure proceedings clouding the title transfer.

Short Sale Negotiations

Eugene statistics show that 40% of short sales succeed as alternatives. Lenders agree to accept less than the full mortgage balance owed. Short sales avoid foreclosure completion while satisfying mortgage company obligations partially.

Banks evaluate hardship circumstances and property values before approving requests. The process requires extensive foreclosure documentation and financial disclosure. Successful negotiations release homeowners from remaining debt after property sale.

Deed in Lieu of Foreclosure

Deed in lieu arrangements follow ORS 86.732 procedures in Oregon. Homeowners voluntarily transfer property ownership to lenders without foreclosure auctions. This option avoids public foreclosure sale while resolving mortgage default situations.

Lenders must agree to accept property instead of pursuing foreclosure regulations. The approach works best when properties have clear title without junior liens. Deed in lieu agreements typically include deficiency balance forgiveness terms.

Need to Sell Your House Fast Before Foreclosure?

Facing foreclosure creates stress and uncertainty about your financial future. Time becomes critical when trying to avoid trustee sales and protect remaining equity. Traditional real estate transactions often take too long when foreclosure deadlines approach.

OR Home Buyers specializes in purchasing properties quickly throughout Eugene and surrounding communities. We are cash home buyers who close transactions in days rather than months. Our team handles properties with title issues, liens, or active foreclosure proceedings.

We serve homeowners in Eugene, Springfield, Cottage Grove, and Junction City needing fast solutions. Our cash offers eliminate financing delays that complicate traditional property sales. We also buy homes in other popular areas of Eugene, OR, providing options when you need them most. Contact OR Home Buyers today to discuss how we can help you avoid foreclosure and move forward with confidence.